After the financial melt-down of 2008, another terrifying event of the global financial crisis is upon us. Like the Lehman crunch its origins lie in the past, perhaps back in the 1990s. But unlike the Lehman situation it is located not in the US but in Europe. We’re talking about the Eurozone crisis. Europe could be on the verge of collapse, but for bankers it is business as usual.

Bankers must come from another planet. Things that surprise and outrage most human beings -- for example, million dollar bonuses paid to thirty-year-old bond traders, transferring billions of dollars across the globe with the click of a mouse -- leave bankers unfazed. They will shrug their shoulders and tell you that you need to pay talent well to keep it, and that such transfers of digital money are just plumbing. Consider the case of Jérôme Kerviel who was convicted in January 2008, just as he turned 31, of losing Euros 4,9 billion for Société Générale through unauthorized derivatives trading. To put this loss in context, it is about the size of the 2010 GDP of Moldova, or four times that of Burundi – and this is real money, belonging to real people. The bank stated that he was working alone and it had happened because of a glitch in their risk control system. So the President of the bank, unlike someone working in any other industry, did not feel it necessary to resign. Bankers just act differently. No wonder the “Occupy Wall Street’ protest movement has spread across the globe.

But occasionally, something will happen in the economy that leave most people somewhat concerned but will strike the fear of God even into the hearts of bankers. Such an event happened on September 15, 2008, when the venerable Wall Street bank Lehman Brothers (founded in 1850) was declared bankrupt despite a feverish weekend spent by officials and bankers in the offices of the New York Fed trying to save it. Most people would have had the attitude that if the bank had taken undue risks acquiring and trading in risky arcane financial instruments such as collateralized debt obligations it did not deserve to survive. They would conclude that the Lehman bankers would lose their jobs and their bonuses, the holders of the bank’s stock would lose their equity, and the world would continue to turn.

But for bankers, and for financial experts working in specialized financial institutions such as the European Central Bank (ECB), the US Fed, the IMF and the World Bank, the Lehman collapse was a terrifying event. It signaled a new nightmarish phase in the global crisis which had started to unfold a year earlier. This new phase was the morphing of the financial crisis into a full-blown credit crisis, far more frightening because it now signaled a loss of confidence in the very financial system itself. It signaled the unwillingness of financial actors and even ordinary people to trust each other in the market. Banks would no longer extend loans, even to trusted clients; viable companies could no longer obtain lines of credit; and the entire economy froze up. For two weeks the world almost ceased to turn, and the economy’s pulse was only resuscitated thanks to the essentially unlimited guarantees provided by governments (especially the US Department of the Treasury) to all actors in the financial markets.

Now the epicenter of the global financial storm has moved to Europe.

European Imbalances

In Europe, several sovereign financial crises emerged at the same time as the sub-prime meltdown in the United States. Icelandic banks were hit (Iceland is not a member of the EU) after extending excessive credit to EU customers, mostly in Britain. In Greece, runaway public spending led to an unsustainable budget deficit and a sovereign debt mountain which could no longer be financed. Irish banks went to the verge of insolvency after lending excessively for real estate, which created a real estate bubble in the Irish Republic, and they needed to be bailed out – and in some cases nationalized – by the government. The crisis spread to Portugal where public spending was also out of hand. The gangrene has now started to nibble at Spain and Italy.

We know very well what happens to most people when they get into financial difficulties, when they lose their jobs and can no longer pay their mortgage. The bank repossesses their home. Companies whose sales are not sufficient to cover their operating costs and service their debt go bankrupt, and the owners lose their ownership capital. But what does it mean for a country to be in financial difficulties?

Unlike a person or a company, a sovereign -- a country -- has additional tools at its service. All governments borrow. They do this by issuing bonds, which are bought by citizens, by local and foreign banks, by pension funds, and sometimes by foreign countries. They borrow to deal with the lumpiness of government expenditure compared to government income (mostly taxes), and to deal with the differing timing between this expenditure and the benefits that accrue to the economy. For example, big infrastructure projects like a motorway require a big outlay at the start, with benefits flowing back to the economy later in the form of decreased transport costs and increased productivity. Spending on educating young people today leads to a more productive labor force tomorrow. This increased productivity, be it from lower transport costs or a better educated labor force, leads to increased output and increased tax revenues, which the treasury uses to pay back the loan with interest.

However, when a country’s spending gets out of hand or its tax revenue declines, it starts to borrow to pay for current expenditure rather than for productive-enhancing investments in the economy. It runs an unsustainable budget deficit and its debt burden starts to creep up. Greece is a textbook case of this process.

Greek Angst

In recent years the Greek government has spent money on things like the Olympic Games and a military buildup that have not contributed to overall productivity. The government holds stakes in assets that could have better been left to the private sector (casinos, ferries, banks, defense companies, the national lottery). Reuters recounts how the civil service has grown increasingly bloated, adding to government expenditure without increasing its revenues. Some of the more egregious excesses cited by Reuters: a bonus for civil servants showing up to work; a dead father’s pension paid to his unmarried daughter (40,000 women benefit at a cost of €550 million); bonuses for using a computer; bonuses for foresters for having to work outdoors.

In addition, there has been widespread tax evasion in all parts of the economy. The Greeks have not been good at paying their taxes, and over the past ten years they have gotten even better at evading them. Tax evasion has become the second national game after football. So with excessive government spending and insufficient taxes, Greek budget deficits ballooned over the decade and successive governments financed their way out by issuing government bonds. The growing mountain of Greek debt started to overshadow the economy.

Even Greek statistics are open to question. The official statistical body of the EU, Eurostat, was forced to issue a caveat in 2009 about the reliability of their budget deficit estimates for the 27 member countries of the EU because of the unreliability of the official Greek figures. At the introduction of the Euro the Greek deficit should have been under 3% of GDP (one of the “Maastricht’ criteria), but has been estimated to have been more like 10%. Greek public debt was above the Maastricht ceiling of 60% to GDP, but the investment bank Goldman Sachs put in place a sophisticated financial instrument which took a portion of Greece’s debt off the country’s books for the Eurozone D-day. This was not technically illegal and Goldman Sachs was never sanctioned for this intervention, which was highly profitable for the bank. But it was most certainly against the spirit of the Maastricht agreement.

Faulty Eurozone mechanisms

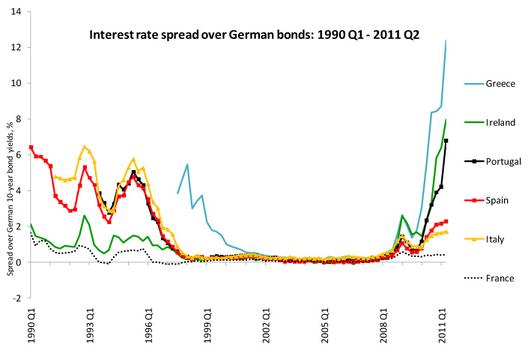

So, how did Greece, Ireland and Portugal get into this situation? Normally as a country’s debts increase, lenders become increasingly wary about lending it more. In order to do so, they need a higher interest rate to persuade them to continue buying government bonds. Higher interest rates give a very powerful signal to the government to rein in its budget deficit, either by cutting expenditure or by increasing taxes or both. Governments also have a powerful tool at their disposal, one that should be used sparingly. If they have their own currency they can devalue, which lowers labor costs compared to the rest of the world and gives a boost to exports, but can lead to higher inflation.

But in the Eurozone, these mechanisms didn’t work. Interest rates for the bonds of individual countries in the zone converged after the introduction of the Euro in January 2002 and remained very similar to one-another until end-2009, despite widely differing levels of productivity, budget and trade deficits, and debt burdens in each of the Euro countries. It was as though the purchasers of the bonds of different Eurozone member countries considered all the countries alike. But of course, they knew well enough that the Southern Europeans were more laid back than the Northerners and had lower overall competitiveness. So in fact the similar treatment implicitly showed their belief that if one country got into macro-economic problems, it would be bailed out by the other member countries. Of course, given the size of their economies, this mainly meant Germany and France.

OECD.stat

Whether Germany and France would indeed bail out Greece, Portugal and Ireland had never been clarified at the time of the introduction of the European currency. Markets (and by this we mean the people and institutions that purchased the bonds of Greece, Portugal and Ireland) assumed that the alternative was simply too unlikely -- the alternative being a Eurozone country defaulting on its Euro-denominated bonds, or leaving the Eurozone altogether and devaluing its currency. But for Germany to support Greece, it would have to accept that the Eurozone had become a Transfer Union. This for most Germans is anathema. So a “zone d’ombre’ was left in the design of the currency, a flaw that has had huge consequences.

The Euro — a doomed love affair

By the way, if you are a technocrat, how could you not love the Euro? It is a wonderful vision – a common currency for the bulk of the European Union countries (17 out of 27 EU members); no foreign exchange aggravation for travelers; promoting intra-Eurozone trade by simplifying the lives of importers and exporters. And in addition, the Euro has become a competitor for the role of global reserve currency played by the US dollar, so Europe is becoming a global financial force to be reckoned with. We can see why the technocrats were fired up by this vision when it was launched at the Maastricht Treaty of 1992. Other European citizens though were rather less enthusiastic.

Unfortunately, creating a common currency comes with a lot of fine print. First, there needs to be a lender of last resort for all banks and sovereigns in the currency zone. Within a country, this role is generally played by the central bank. Second, there needs to be coordinated fiscal and budgetary policy across the entire zone –fiscal federalism. That means that politicians cannot have final say on tax and spending levels within their own countries, and borrowing is carried out Eurozone-wide through issuance of Eurobonds. And third, there needs to be a single pan-Eurozone banking regulator to monitor and enforce common prudential regulations for all banks in the zone, so all banks operate within the same risk framework and have the same capital requirements to backstop their loan portfolios.

In each case, this fine print involves giving up sovereignty to a supranational body, and none of the politicians who signed up to the Euro project wanted to give up more sovereignty to Europe than they had already. They wanted the Euro, but not the fine print. So instead, they replaced these key structural requirements by the “Maastricht Criteria’. For a country to become a member of the Eurozone, in addition to a budget deficit of less than 3% of GDP and a ratio of public debt to GDP below 60%, inflation had to be low and interest rates close to the EU average. Not only were these criteria inadequate to respond to the requirements of a monetary zone, but they were widely flouted at the time of the introduction of the European currency, not only by Greece but also by countries like France. Although a central bank was created to be responsible for monetary policy (the European Central Bank, located in Frankfurt), it was never given the authority to bail out Eurozone banks and countries (the role of lender of last resort). German politicians were concerned that making the ECB the lender of last resort would mean transferring German wealth to poorer Eurozone member countries.

These flaws in the design of the Euro have now come back to haunt us.

The tide goes out on the Euro

Let’s face it -- things seemed to go pretty well with the Euro project for the near decade of growth that occurred following the introduction of the currency on January 1, 1999 (in non-physical form; notes and coins were introduced on January 1, 2002). But bankers have a saying: “it’s only when the tide goes out that you see who is bathing without a swimsuit.’ The financial crisis that struck developed economies in 2007 was the tide receding. Everyone can now see that the Euro was swimming naked. The ECB was constitutionally unable to bail out Irish banks, and when it became increasingly difficult for Greece and Portugal to roll over their short-term debt, the central bank was unable to help them, either. It’s each country for itself, and the devil take the hindmost.

European decision-makers, notably those of Germany and France, initially denied that there was any problem with the Euro. In February 2010 Chancellor Merkel stated that the IMF – specialist in bailing out bankrupt countries – would never operate within the Eurozone. Within a couple of months she had to recant. The IMF, together with the European Commission and the ECB, put together a first bail-out package for Greece, which includes commitments by the Greek government to raise taxes and reduce spending, and is backstopped by financing of €110 billion. The fifth review of the program was undertaken by the joint IMF-European team on October 11, 2011 and concluded that the program was off track. Meanwhile, Greece went into deep recession, rioters took to the streets, and living standards plummeted.

None of this initially made much of an impact on the key decision-makers of the two largest Eurozone countries, Germany and France. Rioting Greeks, plummeting GDP in Ireland, unacceptably high unemployment in Spain – these were not European problems, they were national issues. But as the specter of a Greek default started to loom on the horizon and Greek debt became increasingly risky to hold, it was brought home to the decision-makers that the chief holders of Greek debt, after the Greeks themselves, were German and French banks. Now the crisis was serious and needed a solution, one that would not bring down the banking sectors of the two largest European economies.

Where do we go from here?

There is no easy solution for Europe. The situation is like being the captain of a tanker steaming towards shore, when the engines break down, the rudder becomes stuck, the galley catches fire and the hull springs a leak. The fire in the galley must be doused and the engines fixed, but there is no way to stop the tanker as its momentum drives it onward. It can’t be steered, and it is getting low in the water. If you’re captain, where do you start?

First, tackle the systemic issues of the Euro project. It is now clear to all what the weaknesses in the Euro are. A welcome first step was taken in June 2010 by the creation of the European Financial Stability Fund (EFSF -- essentially a lender of last resort to countries), which has recently been granted some serious financial resources. The EFSF will need to become a permanent European Monetary Fund (EMF) to deal with financial crises in member countries, and for this will need clearer governance rules. (It is currently a “société anonyme registered in Luxemburg). In addition, the Eurozone needs greater control over profligate spending by wayward member countries, as well as a pan-Eurozone banking surveillance mechanism, perhaps as part of the future EMF. President Nicolas Sarkozy and Chancellor Angela Merkel recently announced in August 2011 the creation of the Eurozone Economic Council, but this this body is not credible as it will have only limited authority, and will meet only twice a year.

Second, pity the poor Greeks. They may have been at fault, but decades of experience with IMF programs have convinced me that the Greek government will not be able to implement the IMF program as it is currently designed. It is simply too painful and will tear the country apart. The average income per head has now declined to a level below that of 1980 in real terms, the year Greece became a full member of the EU. Greece must receive some relief, both in terms of the reform program (i.e. reform over a more realistic timeframe) and in terms of debt relief. The reform program must focus much more on regaining competitiveness than simply on raising taxes and cutting costs. Some economists have discussed an exit from the Eurozone for Greece. This is a very scary option with completely unforeseen consequences.

Third, tackle the problems of the banks holding Greek debt (mostly French and German). This debt will eventually have to be restructured, which means that it will never be paid back according to the initial terms of the loan. The earlier the banks recognize that the value of Greek bonds is at most one-half of their initial purchase price and make provisions to offset the resulting loss in capital, the quicker we can all get this crisis behind us. For too long French and German banks, and their authorities, denied that there was any problem and precious time was lost. These banks will now need recapitalizing to make up for the loss of value they will sustain in the process and the Eurozone governments have an important role to play in this recapitalization.

Lastly, and most importantly, the fundamental imbalance in European economies has to be tackled. All the under-performing countries in the Eurozone – Greece, Portugal, Italy, Spain – which have had budget deficits for the entire decade since the introduction of the Euro, must improve their competitiveness, eventually to be on a par with Germany. If they cannot undertake the structural reforms needed they will never manage to balance the public books, and the Euro project will be doomed over the long term. And Germany must accept that in so doing, the huge export market they represent will dry up and German factories must produce goods to be consumed by German consumers or those outside the Eurozone instead.

Whither the Euro? Make no mistake; this crisis will bring changes to Europe. In the best of all worlds, the Eurozone will come out of this crisis stronger, with increased federalism and clearer rules of economic governance. Or alternatively, if European decision makers are not able to rise above their national interests and agree on sensible measures at the level of the Eurozone, it will lead to wrenching dislocation and a lost decade for many member countries, and perhaps even a breakdown of the zone itself.